Registration System for Listed Company Audit Firms

Objectives and Background of the Implementation of the Registration System

The JICPA has conducted the quality control review as part of a self-regulatory function since April 1999 to improve and enhance the quality control system of audit firms that perform financial statement audits. The amendment in 2003 of the CPA Act, which took effect in April 2004, made this quality control review a legally-established system to be monitored by the Certified Public Accountants and Auditing Oversight Board ("CPAAOB").

Although the JICPA took various actions as a self-regulatory body including enhancement of the quality control review structure of the JICPA, corporate scandals involving listed companies relating to financial reporting have emerged one after another since 2004. The scandals took place under circumstances where the Japanese Government has made efforts to achieve a financial policy, "from savings to investment" in the post-bubble period and ensuring confidence in capital markets is becomes more important than ever. The reliability of the CPA auditing system was undermined by the scandals and public confidence in CPA's audits was eroded. Acknowledging the criticism seriously, the JICPA decided to take new actions to further strengthen its quality control review system in order to restore confidence in CPA's audits

The JICPA released, on April 6, 2006, the Chairman and President's Statement announcing the foundation of the Center for Listed Company Audit Firms ("the Center") and introduced the registration system of audit firms that engage in audits of listed companies ("the registration system") as a visible concrete measure, on the basis of a belief that audit quality control should be enhanced not with excessive reliance on the CPAAOB, but through self-regulatory functions.

egistration system of audit firms that engage in audits of listed companies

Fundamental Framework of Registration System Implementation

The registration system has been established under the following fundamental frameworks as part of JICPA's measures to enhance the quality control system of audit firms which perform audits of listed companies by being incorporated into the quality control review system currently conducted by the JICPA.

a. Enhancement of the self-regulatory function (maintenance of indirect regulation)

Ensuring the confidence in audits by CPAs should be accomplished through self-regulation by the JICPA, a professional accountancy body. The role of the government is to monitor the effectiveness of the self-regulation and to provide supplementary oversight as an indirect regulation according to need.

b. Mandatory registration

From the view point of enhancement of the quality control system of firms auditing listed companies which have substantial impact on capital markets, the revised Constitution places an obligation on audit firms subject to the quality control system to be registered with the Center created under the Quality Control Committee.

c. Public accountability

The JICPA demonstrates its commitment to reinforce self-regulatory functions towards the restoration and improvement of confidence in audits by CPAs with an announcement of the implementation of this registration system as a visible concrete measure. Audit firms can also fulfill their public accountability by publishing this information in the overview of their policies and procedures of the quality control system regarding activities for strengthening their quality control.

d. Measures by public disclosure

In the event that significant non-compliance in terms of quality control is identified during the quality control review, measures such as the publication of a summary of the quality control review report or revocation of the registration are imposed on the firms responsible for the non-compliance. These measures are expected to boost members' awareness of their social mission as a CPA.

e. Cooperation with stock exchanges

In order to accomplish the effective function, and to raise public recognition of the registration system, it is critical to ensure that firms with significant identified non-compliance in terms of quality control are virtually unable to provide audit services for listed companies. The JICPA collaborates with market participants such as stock exchanges to ensure effective and proper operation of the registration system.

f. Ensuring fairness and transparency in administration of the registration system

The registration system allows for identification of registered firms whose quality reaches a certain standard, but does not provides assurance for the appropriateness of individual audit engagements. The fairness and transparency of the registration system are to be ensured through the publication of the report of its operation as well as a clear explanation of its objectives to the public so that it may not mislead the public and that it is acknowledged and properly valued.

Ensuring the confidence in audits by CPAs should be accomplished through self-regulation by the JICPA, a professional accountancy body. The role of the government is to monitor the effectiveness of the self-regulation and to provide supplementary oversight as an indirect regulation according to need.

Outline of the Registration System

The following outlines the registration system:

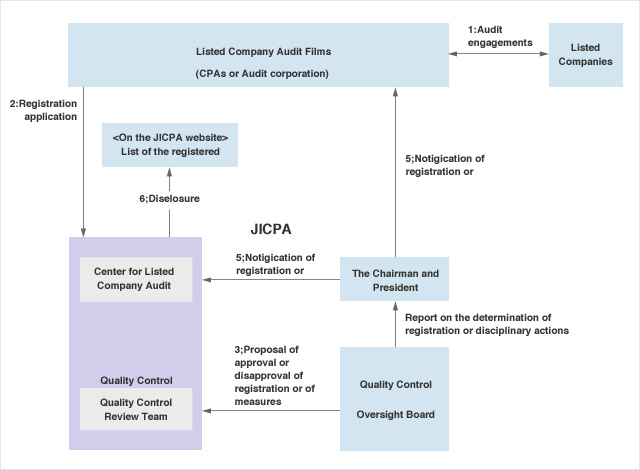

- The JICPA created the Center for Listed Company Audit Firms ("the Center") under the Quality Control Committee to administer the overall registration system.

- The revised Constitution requires audit firms which audit listed companies (hereinafter referred to as "registered audit firms") to register with the Center.

In order to avoid excluding non-registered audit firms from initiating audit services to listed companies, a category of "associate registered audit firms" was established. -

Applicant audit firms submit the following documents and declaration to the Center:

- Application form;

- Accompanying documents describing the overview of the audit firm (fundamental information on the firm is to be publicly available);

- Overview of policies and procedures of the quality control system of the audit firm (to be put on the publicly-accessible register); and

-

A declaration describing the firm's agreement of:

- Adherence to the policies and procedures of the quality control system;

- Compliance with requirements imposed on registered audit firms, including faithful responses to recommendations made as a result of the quality control review;

- Acceptance of any measures imposed on the audit firm for failure to adhere to the requirements; and

- Acknowledgement that information and the declaration of the registered audit firm will be put on the publicly-accessible register

-

The Quality Control Committee proposes to the Quality Control Oversight Board whether to approve an application or not after consideration of the application based on past results of quality control reviews. The majority of members of the Quality Control Oversight Board consist of knowledgeable persons outside the profession. The Quality Control Oversight Board deliberates the proposal and makes the determination. The screening application criteria are:

- Upon the inception of this system, audit firms that audit listed companies are registered after the screening of the application documents. However, those audit firms are subject to urgent reviews of improvement in matters identified in past quality control reviews and compliance with the Standards on Quality Control for Audits, applicable for periods ended on March 31,2007.

- Once the operation of this system starts, the quality control review should be conducted for applicant audit firms and then the conclusion is then reached based on certain screening criteria.

-

The Constitution was revised so that the JICPA can take the following measures when non-compliance of a registered audit firm is identified during the course of a quality control review:

- Admonish the firm and require additional CPE credits (to be nonpublic);

- Publish a summary of the qualified items identified during the quality control review (to be put on the publicly-accessible register); and

- Revocation of registration and publishing the facts (to be put on the publicly-accessible register)

e latter two measures are imposed when significant non-compliance is identified. Such significant non-compliance includes a qualified conclusion with a significant qualified item or an adverse conclusion, or refusal of or non-cooperation with a quality control review.

- Measures including a revocation imposed on a registered audit firm are proposed by the Quality Control Committee, and the Quality Control Oversight Board then deliberates the proposal and makes the determination. The decision of the Quality Control Oversight Board is notified to the audit firm in writing by the Chairman and President. However, the determination of revocation is delivered directly to the audit firm.

-

Names of unregistered audit firms and reasons for which those firms are not registered with the Center will be published. Reasons may include:

- The audit firm has not yet applied for the registration;

- The audit firm did apply, but the application was not approved; or

- The registration of the audit firm was revoked

- The JICPA seeks cooperation with market participants such as stock exchanges in order to ensure the appropriate operation of this system. Doing so ensure that an audit firm which has serious non-compliance in terms of quality control is unable to provide audit services to a listed company.

The Role of Organizations that Administer the Registration System

The registration system is intended to encourage the improvement and enhancement of the quality control system of registered audit firms through measures such as the publication of the summary of qualified items identified during the quality control review and revocations imposed on registered audit firms with non-compliance identified in the quality control review. The registration system is operated by the organization that conducts the quality control review for the JICPA.

The Center for Listed Company Audit Firms

The Center for Listed Company Audit Firms ("the Center") has been created under the Quality Control Committee. Registered audit firms belong to this Center. The Center has the following duties and responsibilities that are executed by the Secretariat under the supervision of the Quality Control Committee:- Acceptance of application;

- Preparation and maintenance of the register (including acceptance of request to view the register);

- Acceptance and custody of submitted documents including overviews of quality control systems and declarations;

- Acceptance of regular reports and changes to information from registered audit firms;

- Controls and maintenance of registration computer system; and;

- Other matters relating to the register.

- Quality Control Committee

The Quality Control Committee examines registration applications and considers necessary measures against a registered audit firm that demonstrate non-compliance based on past quality control reviews. The Quality Control Committee then submits a proposal of approval or disapproval to the Quality Control Oversight Board. - Quality Control Oversight Board

The Quality Control Oversight Board deliberates on the approval or disapproval of registration or of measures submitted by the Quality Control Committee and makes the appropriate determination.

Members of the Quality Control Oversight Board formerly consisted of knowledgeable persons outside the profession (except for one member who was a CPA) as the Board's responsibility is to monitor the quality control review conducted by the Quality Control Committee. Taking into consideration the additional responsibilities described above, the composition of members of the Board was re-examined in view of the emphasis on expertise. The number of members was also increased to eight: five knowledgeable persons outside the profession and three CPAs. - Reporting to the CPAAOB

With respect to the operation of the registration system, the Quality Control Committee submits regular reports to the CPAAOB as part of the quality control review. Through independent monitoring by the CPAAOB, the JICPA believes that the objectives of the registration system will be achieved more effectively and appropriately.